TL;DR: A HECM reverse mortgage lets homeowners 62+ convert home equity into a lump sum — with no monthly payment and no tax consequences — making it one of the most effective tools for funding a living inheritance, including a down payment gift to an adult child.

“The Money Will Mean More to Her Now Than When I Die”

A client said that to me recently. She wants to pull $200,000 out of her home equity to help her daughter buy a house. And she’s not doing it out of desperation — she’s doing it as a deliberate financial decision. No monthly payment coming out of her pocket. No tax consequences like she’d face pulling from her investment portfolio. Just her home equity, converted into something her daughter can use right now.

The Wall Street Journal just reported that older Americans are sitting on $110 trillion in wealth — more than any other generation in history. But here’s the problem: because people are living longer, that inheritance may not arrive until the kids are in their 60s. What does a down payment mean to a 65-year-old?

She’d rather her daughter have it at 35. And she gets to see it make a difference.

Why a Reverse Mortgage — Not a Portfolio Withdrawal

This is the part financial advisors and CPAs need to understand, because the decision between funding a gift from a portfolio versus a HECM reverse mortgage isn’t just about liquidity — it’s about tax efficiency and cash flow.

No tax consequences. A HECM lump sum is loan proceeds, not income. It doesn’t appear on a 1040. Compare that to liquidating a brokerage account or taking an IRA distribution, which can trigger capital gains, ordinary income taxes, and potentially push the borrower into a higher Medicare premium bracket (IRMAA).

No monthly payment. Unlike a home equity loan or HELOC, a reverse mortgage has no required monthly payment. The loan balance accrues and is settled when the home is eventually sold — which means the borrower’s cash flow stays intact.

The home stays in the family’s hands. She’s not selling. She’s not downsizing. She’s tapping an asset she’s spent decades building, on her own timeline.

The “Great Wealth Trickle” Is Already Happening

The WSJ piece frames this well. The great wealth transfer — the $110 trillion that’s supposed to pass from boomers to their children — is on hold, because boomers are living longer. But what’s happening instead is a “great wealth trickle”: smaller, intentional gifts given now, while parents are alive to see the impact.

One retiree in the piece put it plainly: “They can use the money now more than we can use it to watch our stock portfolio go up.”

A reverse mortgage is one of the most efficient mechanisms for that trickle — particularly for homeowners who are equity-rich but cash-flow-conscious. If your client has a paid-off or nearly paid-off home and an adult child struggling to break into today’s housing market, this is a conversation worth having. For more on how HECM proceeds are calculated, see my breakdown of reverse mortgage principal limits.

What This Looks Like in Practice

For a homeowner in their late 60s or 70s with significant equity, a HECM can often generate a lump sum of $150,000–$300,000 or more, depending on age, home value, and current interest rates. That’s a meaningful down payment in most markets — including West Seattle, where entry-level homes regularly require $80,000–$150,000 down to compete.

The borrower stays in their home. No payment goes out the door each month. And the gift is funded from an asset class — home equity — that would otherwise sit dormant until the estate is settled.

FAQ

Can you use a reverse mortgage to give money to your kids?

Yes. Reverse mortgage proceeds are yours to use however you choose — including gifting a down payment to an adult child. The funds are not restricted to personal expenses.

Is a reverse mortgage lump sum taxable?

No. HECM loan proceeds are not considered income and are not reported on your tax return. This is one of the key advantages over liquidating a portfolio to fund a gift.

Does a reverse mortgage have monthly payments?

No monthly payment is required. The loan balance accrues interest and is repaid when the home is sold, the borrower moves out, or the estate is settled. Borrowers must continue to pay property taxes, insurance, and maintain the home.

What is a living inheritance?

A living inheritance is a financial gift given while the donor is still alive — allowing them to see the impact of their generosity rather than passing assets through an estate. With people living longer, adult children may not inherit until they’re in their 60s, making the timing of a traditional inheritance less meaningful.

If you have a client who’s equity-rich and thinking about how to help their kids, send them my way. It’s worth a conversation.

A mortgage broker and agent reviewing a condo project's warrantability together.

TL;DR: The March 2026 condo rule changes from Fannie Mae and Freddie Mac (Lender Letter LL-2026-03) make condos easier to finance in three ways and harder in two. A non-warrantable condo is a building the agencies won’t finance, and the two tightening changes will push more buildings into that bucket starting August 3, 2026. Before you list a condo or write an offer, send me the project name, city, and state and I’ll tell you exactly where it stands.

What is a non-warrantable condo?

We’re all used to checking whether a condo is FHA approved. That part hasn’t changed: FHA still keeps a public approved-condo list. If the project isn’t on it, an FHA loan is off the table unless you pursue a single-unit approval. (Worth knowing when you’re weighing FHA vs conventional for a buyer.) But more and more frequently the bigger problem isn’t FHA. It’s that Fannie Mae and Freddie Mac are disapproving condo buildings for conforming loans.

A non-warrantable condo is a project that doesn’t meet Fannie or Freddie eligibility, so the agencies won’t buy a loan secured by a unit in it. When that happens, conventional financing dries up for every unit owner in the building, not just one borrower. A condo can be non-warrantable for a long list of reasons. Too much commercial space, one entity owning too many units, litigation against the HOA, pending special assessments, underfunded reserves, low owner-occupancy on a prior-standard file, or insurance that misses the HOA master-policy requirements. Fail one criterion and the whole project is out.

Here’s the part that catches agents off guard: a building can look perfectly normal, sell fine last year, and still be non-warrantable today. The borrower’s credit and down payment don’t fix it. The project itself has to qualify.

3 ways condos are getting easier (and 2 ways they are getting harder)

On March 18, 2026, Fannie Mae issued Lender Letter LL-2026-03 and Freddie Mac issued a matching bulletin. These are the most significant changes to condo underwriting since the agencies started tightening after the Surfside collapse in 2021. The simplest way to hold it all in your head: condos get easier to finance in three ways, and harder in two. Three of the changes are already live. The two that tighten things arrive on set dates you can put on your calendar.

Easier: 3 changes that took effect immediately

All three of these are already in force, and each one puts buildings back in play that conventional financing had shut out:

1. Investors can buy again. The old rule required 50% owner-occupancy for an investment-property loan under full review on an established project. That threshold is gone. It unblocks a lot of urban and rental-heavy buildings.

2. Insurance requirements loosened. Lenders can now lean on Guaranteed Replacement Cost or Extended Replacement Cost to satisfy coverage sufficiency. Inflation guard is no longer required, and roofs and certain property qualify on an actual-cash-value basis. Buildings the agencies previously flagged “unavailable for lending” over insurance can return to eligible.

3. More projects qualify with less red tape. Waiver of Project Review now reaches established condo projects with 10 or fewer units (no master association, no condotel activity). And Florida new construction no longer needs mandatory PERS submission, so lenders can review those projects under standard new-construction review types.

So if you’ve got a deal that died on a condo last year over insurance or investor mix, it’s worth a second look. It may be financeable now. The two changes below cut the other way.

The 2026 condo rule changes arrive on set dates — August 3, 2026 and January 4, 2027.

Harder: 2 changes coming on set dates

Both of these tighten the screws, and both land on dates you can put on the calendar right now:

1. Limited Review goes away — August 3, 2026. For loan applications dated on or after that day, Fannie and Freddie eliminate Limited and Streamlined Review for established projects with more than 10 units. Every one of those loans moves to Full Review.

2. Reserves get stricter — August 3, 2026 and January 4, 2027. Starting August 3, lenders must use the highest recommended reserve allocation in the study, not a baseline number. Then on January 4, 2027, the minimum annual reserve contribution rises from 10% to 15% of budgeted assessment income.

The first one is the gut punch. Limited Review was the fast lane: if a buyer put enough down (often 10% on a primary), the lender could approve the loan by verifying basic property and insurance data without digging into the association’s full financials. Industry estimates put 40% to 65% of current condo loans in that lane. Closing it means more documentation, more HOA paperwork, and longer underwriting on a huge share of condo files. The borrower’s down payment no longer changes that.

It also costs more. Full Review leans on a full lender condo questionnaire completed by the HOA or its management company, and those carry a fee the buyer usually pays. A standard or limited questionnaire often runs around $75 to $150, but the full lender version typically lands in the $200 to $350 range, and sometimes higher, with rush fees of $50 to $100 on top if the file is on a clock. Many associations route these through third-party providers like CondoCerts or their management company, so the cost and the turnaround are out of your hands once the request goes in. With Limited Review gone, more files will trigger that full questionnaire, which means more upfront cost and more waiting on the association before a deal can close.

The reserve changes hit the building, not the borrower. For a lot of HOAs, getting to 15% means an owner vote and higher dues. Read all of this as a timeline, not a checklist. A condo that sails through in spring 2026 may need more documents by late summer and may stumble on reserves in early 2027. The same building, three different answers depending on the application date.

As a broker, non-QM and portfolio options can finance condos that conventional loans can’t.

How do you check if a condo is warrantable before you list it?

You don’t have to guess. Send me the condo name, city, and state of any project you’re about to list or that your buyer is eyeing. I’ll look up its status. We can catch a non-warrantable problem early instead of three days before closing. It’s the same reason I tell agents to vet a pre-approval up front.

And here’s why I’m a broker and not a single-bank loan officer: when Fannie and Freddie say no, I’m not done. I work with tens of lenders that have non-QM condo products with different rules, different options, and different pricing. A building that’s non-warrantable for conventional financing is often perfectly financeable elsewhere. A portfolio or non-QM lender underwrites the project differently. That’s the whole point of having options. One door closes, I’ve got a dozen more to try for your client.

FAQ

What is the difference between a warrantable and non-warrantable condo?

A warrantable condo meets Fannie Mae and Freddie Mac project eligibility, so it qualifies for conventional financing. A non-warrantable condo fails one or more of those criteria, so the agencies won’t back a loan on it. Non-warrantable units typically need a portfolio or non-QM loan instead, often with different down payment and pricing terms.

Does a bigger down payment fix a non-warrantable condo?

No. As of August 3, 2026, the end of Limited Review means a larger down payment no longer replaces a full project review. Approval depends on whether the condo project meets Fannie and Freddie standards, not just the borrower’s equity or credit strength.

Can you still get a loan on a non-warrantable condo?

Yes, often through a non-QM or portfolio lender. These lenders underwrite the project under their own guidelines instead of Fannie or Freddie rules. As a broker I work with many of them, so a building that’s off-limits for conventional financing can still have a path. Terms and pricing vary by lender and project.

Is a non-warrantable condo the same as a condo that isn’t FHA approved?

No. FHA approval is a separate HUD list for FHA loans. “Non-warrantable” refers to Fannie Mae and Freddie Mac conventional eligibility. A condo can be FHA approved but non-warrantable for conventional, or the reverse, so check both depending on the loan type.

If you have a client weighing a condo and you’re not sure where the building stands, send the project my way and I’ll check it before it costs anyone a contract.

Don’t just take my word on condo financing

If you want a read on how I work with clients before sending one my way, here’s where past borrowers and partners have weighed in:

TL;DR: The reverse mortgage principal limit is the percentage of your client’s home value they’re allowed to borrow against. For a HECM, only two inputs matter to ballpark it: the youngest borrower’s age and the home value. No credit pull, no income docs, no tax returns. Proprietary reverse mortgages follow the same logic but stretch the limits for higher-value homes. If you can ask the age and a Zillow estimate, you can tell a client in 30 seconds whether the math is worth a real conversation.

What the reverse mortgage principal limit actually is

The reverse mortgage principal limit is the dollar amount your client is allowed to draw, in total, against the equity in their home. Think of it as the borrowing ceiling. It’s expressed as a percentage of home value (HUD calls that the principal limit factor, or PLF), and it gets set up front based on two inputs: the age of the youngest borrower and the home’s appraised value. That’s it. No credit score, no W-2s, no DTI calculation just to see if the deal pencils.

This is the part that surprises advisors and CPAs the most. We can run a real, useful first-pass conversation with a client based on age and a property estimate. If the math doesn’t work, we know in five minutes and nobody wastes anyone’s time. If it does work, then we move into the actual application — financial assessment, counseling, the works. (For condo clients specifically, there’s also a separate HOA checklist worth walking through before the principal limit conversation gets very far.)

How HECM principal limits get calculated

For a Home Equity Conversion Mortgage — the FHA-insured product most reverse mortgage clients end up in — the principal limit factor comes from a HUD-published table. Two variables feed it:

Age of the youngest borrower (or non-borrowing spouse). Older = higher PLF. A 62-year-old gets a lower percentage than an 82-year-old, because the loan is expected to compound over fewer years.

Expected interest rate. Lower expected rates mean a higher PLF. Higher rates compress the percentage your client can access.

The home value matters too, but it’s not in the PLF formula itself — it’s the multiplier. The PLF is a percentage; the home value (capped at the FHA lending limit, currently $1,249,125 for 2026) is what it gets multiplied by. So a 75-year-old with a $600,000 home and a 70-year-old with a $600,000 home get different dollar amounts even though the home value is identical.

One nuance worth knowing: HUD revises the PLF tables when interest-rate conditions shift materially. The percentages aren’t static. What looked like a 50% PLF for a borrower last year might be a few points different now. We always quote off current numbers, never a stale table.

Where proprietary reverse mortgages change the math

Proprietary reverse mortgages — sometimes called jumbo reverse mortgages — are the lane for clients whose home value exceeds the HECM lending limit. They’re privately insured (not FHA-backed), and the principal limit math gets recalibrated for higher property values.

Three things shift:

The home value ceiling lifts. Some proprietary products go up to $4 million or more in eligible value. The HECM cap of $1,249,125 disappears.

Minimum age may drop. A few proprietary products go down to age 55 instead of 62. Useful for clients still working but planning a retirement transition.

The PLF curve looks different. Each proprietary investor sets its own table. Some are more generous than HECM at the high end; others are more conservative. Always quote both side by side when the home value is in the overlap zone.

For a $1.8 million home owned by a 70-year-old, the HECM caps out using the FHA lending limit — the borrower’s home value above $1,249,125 effectively doesn’t count. A proprietary product can underwrite against the full value. That gap is the entire reason proprietary exists.

Why this is a low-friction first conversation for your client

If you have a client who’s curious whether a reverse mortgage solves something — paying off an existing forward mortgage, opening a standby line of credit, funding long-term care without selling appreciated assets, or funding the renovations that let them age in place — the first question isn’t “will they qualify.” It’s “do the numbers work.”

Because the principal limit calculation skips credit and income, we can answer that question without pulling credit, without asking for tax returns, and without the client feeling like they’ve started an application they can’t back out of. Two pieces of info, one phone call, and your client knows whether to keep going.

The three questions I usually get back from advisors after that first conversation:

Can the principal limit pay off the existing mortgage with room to spare? (If yes, monthly payment obligation goes away.)

What does the line of credit look like five or 10 years out, given the growth feature on unused HECM credit? (Most advisors are surprised by this number.)

Does it make sense to set this up now, before rates or HUD tables move, even if the client doesn’t need to draw yet?

None of those need a credit pull to answer at the napkin-math stage.

What your client receives with a principal limit estimate

When I run a principal limit, the client doesn’t get a wall of numbers — they get an interactive presentation built around their own scenario. The fastest way to understand what that looks like is to see one. Here’s a fully interactive example built on a sample scenario (a 71-year-old borrower, ~$869K home):

It walks through the gross principal limit and how it’s derived, what gets paid off at closing, the line of credit that’s left over, and — the part advisors tend to linger on — a slider that shows how the unused line of credit grows year by year. There’s also a build-your-own amortization tool where you can model draws, voluntary payments, and different appreciation assumptions across 30 years. That’s the same output your client gets, personalized to their age, home value, and existing mortgage.

What to send me to get a real number

If you want me to run a principal limit for a client, send three things and I’ll have a quote back same day:

Date of birth of the youngest borrower (and non-borrowing spouse if applicable)

Estimated home value (Zillow, Redfin, or recent appraisal — we’ll order a real appraisal later)

Approximate balance on any existing mortgage

That’s the full intake to get a written principal limit estimate, an amortization, and a line-of-credit projection — delivered as an interactive presentation like the example above. The full application — counseling certificate, financial assessment, title work — only happens after the client sees the numbers and wants to move.

FAQ

What is the principal limit on a reverse mortgage?

The principal limit is the maximum amount a reverse mortgage borrower can draw against their home’s equity. For a HECM, it’s calculated as a percentage of the home value (the principal limit factor, or PLF) based on the youngest borrower’s age and the expected interest rate. The home value used is capped at the FHA lending limit, currently $1,249,125 for 2026.

Does a reverse mortgage require a credit check?

Not to calculate the principal limit. We can quote a number based on age and home value alone. Credit and income come into play later, during the financial assessment step of the full HECM application — but only after the client has seen the numbers and decided to move forward.

How is a proprietary reverse mortgage different from a HECM?

A HECM is FHA-insured and capped at a home value of $1,249,125 for 2026. A proprietary reverse mortgage is privately insured, often allows home values up to $4 million or more, and may start at age 55 instead of 62. The principal limit percentages differ between products, so for high-value homes it’s worth quoting both side by side.

What age does a borrower need to be to qualify for a reverse mortgage?

62 for a standard HECM. Some proprietary reverse mortgages go down to 55. The youngest borrower (or non-borrowing spouse) determines which age is used for the principal limit calculation.

Why does the principal limit go up with age?

The loan compounds over the borrower’s remaining time in the home. An older borrower has a shorter expected horizon, so HUD’s PLF tables let them borrow a larger share of equity up front without the loan balance running past the home value over time.

If you have a client weighing a reverse mortgage and want to read how I work with referral partners before sending one my way, here’s where past borrowers and partners have weighed in:

VantageScore mortgage approvals are here. Fannie Mae, Freddie Mac, and lenders like UWM now accept VantageScore 4.0 on conventional loans. Brokers can pull both FICO and VantageScore on the same credit report and use the higher of the two. That means the Credit Karma score your client checks on their phone is finally relevant to their home loan — and for borrowers near a pricing tier breakpoint, with thin files, or with old medical collections, it can change qualifying and rate.

The “but Credit Karma says…” conversation just changed

If you’ve worked with buyers for any length of time, you know the conversation. I pull credit, I give them their score, and they say: “Wait — Credit Karma says I’m a 740.” Then I explain that FICO and VantageScore are two different scoring systems, and Fannie and Freddie don’t use VantageScore for mortgage lending.

That second part isn’t true anymore. This year, Fannie Mae and Freddie Mac validated VantageScore 4.0 for mortgage lending. UWM — along with a short list of other approved lenders — now pulls both FICO and VantageScore on every credit report. Brokers use whichever score gives the borrower a better outcome. No extra cost. No extra steps.

This is genuinely new. Only a handful of lenders have it right now, and the broker channel got it first. So when your client asks why their Credit Karma score doesn’t match the lender’s score, the answer is no longer “they’re different systems and we don’t use that one.” The answer is now “we can use that one — and there are real situations where it’ll help.”

What is a VantageScore, and why is it different from FICO?

VantageScore is a credit scoring model the three credit bureaus — Equifax, Experian, and TransUnion — built as a competitor to FICO. The current version is VantageScore 4.0. It uses the same 300-850 range as FICO, but it weighs the underlying credit factors differently and includes a few things FICO doesn’t.

Three differences that matter for your clients:

Trended data. VantageScore 4.0 looks at up to 24 months of balance and payment patterns, not just a snapshot. A borrower paying balances down over time looks better than the same balance held flat.

Thinner files score. FICO needs at least six months of credit history to generate a score. VantageScore can score someone with as little as one month of credit activity. That matters for younger buyers, recent immigrants, or anyone rebuilding.

Medical collections don’t count. VantageScore 3.0 and 4.0 ignore medical collection accounts entirely, regardless of amount or whether the borrower paid them. The mortgage-specific FICO models we’ve used for decades — Equifax Beacon 5.0, Experian/Fair Isaac V2, TransUnion Classic 04 — treat a medical collection the same as a credit card charge-off.

That last point is worth pausing on. The CFPB tried to ban medical debt from credit reports entirely in early 2025. A federal court struck down the rule that July. So medical collections over $500 still hit credit reports, and the older mortgage FICO scores still hammer borrowers for them. VantageScore does what the regulation couldn’t.

Why Credit Karma matters for VantageScore mortgage approvals

Credit Karma displays a VantageScore — specifically VantageScore 3.0, from TransUnion and Equifax. It’s not the exact same model the lender uses (mortgages pull VantageScore 4.0 across all three bureaus). But the philosophy and weighting sit far closer to each other than either does to FICO.

For years, that Credit Karma number was background noise in the mortgage conversation. We had to explain it didn’t count. Now it counts. The directional read — “my score is around here” — is now useful information for qualifying and pricing.

A 741 on a credit-monitoring app used to be background noise. With VantageScore now accepted in mortgage pricing, that number finally has weight.

Where a higher VantageScore mortgage tier actually changes the deal

Three scenarios where pulling both scores and using the higher one moves the needle:

A borrower sitting just below a pricing tier breakpoint

The Fannie and Freddie loan-level price adjustment grid has hard breakpoints at 720, 740, 760, and 780. A buyer at 736 FICO sits in a worse pricing tier than a buyer at 742. If their VantageScore comes back at 745 or 750, we just jumped a tier. Same loan, same down payment, materially cheaper money — either lower rate at the same cost, or lower costs at the same rate. This is the same kind of structural pricing improvement we covered with the UWM 1.0 buydown. A small change in the inputs translates to real dollars at the closing table.

LLPA pricing tiers have hard breakpoints at 720, 740, 760, and 780. Crossing one changes the math on every dollar of the loan.

A borrower with old medical collections

Say your client has a $1,500 hospital bill in collections, dragging their mortgage FICO down 40 or 50 points. Their VantageScore will look very different — because VantageScore ignores it entirely. For a borrower who’s otherwise clean, that single change can flip them from “barely qualifies” to “qualifies at a normal rate.”

A thin-file borrower

Young buyers, recent immigrants, anyone whose credit history is short and sparse — these are the borrowers who often hear “come back in six months once you have more history.” VantageScore can score them today. Working out of West Seattle, I see this often: first-time buyers in their late twenties, one credit card, steady job, 5% down payment ready to go. The only thing holding them back is a FICO thin enough that they got told no last year. That’s exactly the borrower VantageScore was built to evaluate. Worth checking against the FHA vs. conventional decision too, since a higher VantageScore can shift which loan type prices best.

Why VantageScore mortgage adoption matters for your clients (and your business)

For real estate agents: when a buyer with marginal credit sits on the sidelines, this is a reason to send them back through pre-approval. The answer they got six months ago — even three months ago — may not match the answer they get today. I see this most often with West Seattle, Burien, and South King County buyers who got an early “no” before VantageScore was on the table. For a fuller list of what to ask a lender during that conversation, see questions to ask a lender about a pre-approval.

For financial advisors: clients who are reverse-mortgage-curious, refinance-curious, or buying a second home — and assuming their score won’t qualify them at a good rate — may now have a path they didn’t before. Worth a conversation, especially for clients whose medical history has quietly suppressed their FICO. If you’re not sure which loan type fits, that’s worth a 15-minute call.

The competitive piece: this is a broker-channel advantage right now. Retail banks tend to move slower on new models. Most are still building their internal approval workflow. A solo broker working with UWM has dual-score pricing today. That’s a real reason for your client to call a broker before walking into their bank.

The honest caveats of VantageScore mortgage adoption

A few things to keep front of mind so you can manage expectations:

Credit Karma uses VantageScore 3.0. The mortgage version is 4.0. They’re related but not identical, so the Credit Karma number won’t match the mortgage VantageScore exactly.

Credit Karma pulls TransUnion and Equifax. Mortgage credit pulls all three bureaus and uses the middle score. So a high Credit Karma reading is encouraging but not a guarantee.

UWM and other approved lenders apply a conservative haircut to the VantageScore before pricing — a guardrail while the new model gets tested at scale. The borrower’s VantageScore typically needs to land meaningfully higher than their FICO to actually change the pricing tier.

This is conventional-loan territory right now. FHA acceptance is announced but rolls out separately. Government-loan adoption sits on a slower timeline.

Underwriting standards haven’t loosened. Documentation, debt ratios, reserves — all the same. This is a pricing and qualifying optimization, not a relaxation of standards.

FAQ

Is VantageScore accepted for mortgage loans now?

Yes — for conventional loans. The FHFA validated VantageScore 4.0 for use by Fannie Mae and Freddie Mac, and approved lenders like UWM now pull both FICO and VantageScore on every file. FHA acceptance has been announced and rolls out separately. VA and USDA timelines are still in progress.

Will my Credit Karma score match what the VantageScore mortgage lender sees?

Not exactly. Credit Karma shows VantageScore 3.0 from TransUnion and Equifax. Mortgage credit pulls VantageScore 4.0 from all three bureaus, uses the middle score, then applies a conservative haircut before pricing. The Credit Karma number is now a useful directional read. It isn’t the final mortgage number.

Does VantageScore ignore medical collections?

VantageScore 3.0 and 4.0 ignore medical collection accounts entirely, regardless of the amount or whether the borrower paid them. The mortgage-specific FICO models still count them. For a borrower with a medical collection on file, that single difference can swing their qualifying score meaningfully.

Who benefits most from VantageScore in mortgage lending?

Three groups: borrowers sitting just below a pricing tier breakpoint, borrowers with medical collections on their report, and thin-file borrowers like first-time buyers, younger borrowers, or recent immigrants who don’t yet have six months of credit history.

Does using VantageScore cost the borrower anything extra?

No. With UWM’s current rollout, both FICO and VantageScore come back on the same credit pull at no additional cost to the borrower or broker. We use whichever gives the better result.

Don’t just take my word on VantageScore mortgage approvals

If you want a read on how I work with clients before sending one my way, here’s where past borrowers and partners have weighed in:

If you have a client whose Credit Karma score has always run higher than what lenders quote them, send them my way. We can pull both scores at no cost and see if there’s a path that wasn’t there six months ago.

UWM's Free 1-0 Buydown promotion — currently funded by the lender at no out-of-pocket cost to the buyer.

UWM is paying for a 1-0 temporary buydown right now. It drops a buyer’s first-year mortgage rate by a full percentage point. No out-of-pocket cost. On a $600,000 loan, that’s about $280 a month, or roughly $3,400 across the first 12 months. There’s a real trade-off: a slightly lower permanent rate exists without the buydown. The break-even between the two is around 3.5 years. The 10-year Treasury is back near where it was a year ago. The odds of a refinance window opening before then are good. For a West Seattle or Burien buyer stretching to make a $600,000 purchase work, that first-year breathing room can be the difference between buying now and waiting twelve months.

UWM’s Free 1-0 Buydown promotion — currently funded by the lender at no out-of-pocket cost to the buyer.

What the UWM 1-0 Buydown Actually Does

UWM is running an aggressive promotion. It’s a “Free” 1-0 temporary buydown they fund out of their own pricing margin. The mechanics are simple. For the first 12 months, the buyer pays as if their rate is 1% lower than the note rate. In Year 2 through Year 30, the full note rate kicks in. The subsidy sits in an escrow account at closing and pays the difference each month during Year 1.

UWM is funding the buydown. It does not come out of the buyer’s pocket. It does not eat into a seller credit. It does not require any negotiation in the purchase contract. From a buyer’s cash-to-close perspective, it is genuinely free.

How Much Does It Save in Year One?

On a $600,000 loan, the 1-point rate reduction is worth roughly $280 a month in lower principal and interest. Over 12 months that totals around $3,400. Real affordability relief in the first year — when buyers are also absorbing moving costs, furniture, and repairs that nobody quotes them on the GFE.

For a buyer on the fence because the monthly payment was just outside their comfort zone, this changes the math. It reframes what’s actually affordable in the first year of ownership.

Where’s the Catch? The Real Trade-Off Against the Permanent Rate

Calling it Free is technically accurate from the buyer’s side. It is not free in the absolute sense. UWM is spending pricing margin on the Year 1 subsidy that could otherwise have gone toward a slightly lower permanent rate. On the same rate sheet, the same buyer can typically lock about a quarter-point lower rate for the full 30 years. No buydown, no Year 1 cushion. Just a permanently cheaper payment.

So the choice is a real trade-off. Year 1 cushion versus permanent monthly savings over the life of the loan. Anyone telling a buyer it is a no-brainer either way is oversimplifying.

The break-even point: hold the loan past about 3.5 years and the lower permanent rate beats the buydown.

When Does the UWM 1-0 Buydown Win?

The break-even between the buydown and the lower permanent rate works out to roughly 3 years 7 months. If the buyer refinances or sells before then, the buydown wins. If they hold the loan past that point, the lower permanent rate pulls ahead. And stays ahead for the rest of the term.

The math is straightforward. The buyer banks about $3,400 in Year 1 with the buydown. Then they pay roughly $110 a month more than they would have on the lower permanent rate, every month after that. Those $110 chunks chew through the $3,400 head start over about 31 months in Year 2 onward. Total time to break even: 12 plus 31, or 43 months.

Why a Refi Window Inside 3.5 Years Is More Likely Than Not

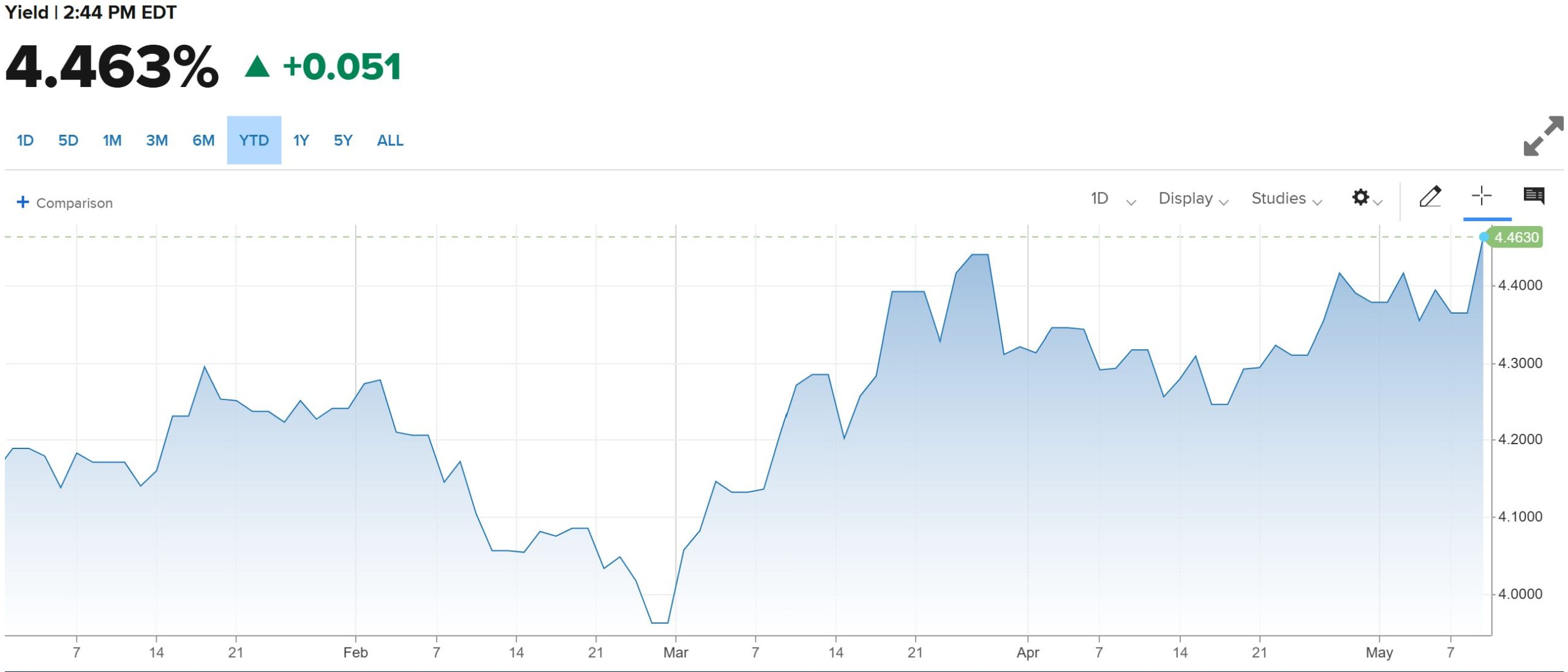

This is where the timing question matters. The 10-year Treasury drives mortgage rates more than any other single input. It closed at 4.46% as of mid-May. That’s up from a late-February low near 3.97%. That’s roughly half a percentage point of upward move in about ten weeks. It puts the 10-year right back near where it was a year ago.

10-Year Treasury YTD 2026: up from a late-February low near 3.97% to 4.46% in mid-May — almost half a percentage point of upward move in about ten weeks.

The directional implication is simple. There’s real room for the 10-year to fall back toward that February low. That happens if economic data softens or the Fed signals more accommodation. Most major forecasters expect 30-year fixed rates to drift lower through late 2026 and into 2027. That includes the Mortgage Bankers Association and Fannie Mae. Whether the move is gradual or sharp depends on the data, but the directional consensus is clear.

For a buyer choosing between the buydown and the lower permanent rate, that backdrop tilts the decision. A refinance opportunity opening in the next 24 to 36 months is more likely than not. That’s well inside the 3.5-year break-even window where the buydown wins.

How to Frame the Math for a Client on the Fence

The buyer needs three pieces of information to make this decision. None of them are about the buydown itself:

How long they realistically plan to hold the loan. The median U.S. homeowner stays put for 11.8 years. But the average mortgage only lives 5 to 7 years — because refinances end loans too. If they refi inside 3.5 years, the buydown wins.

What their cash-flow priorities look like in Year 1 specifically. First-year homeownership tends to be the most cash-strained year for any new owner — especially for Puget Sound buyers absorbing property taxes that are higher than what their lender estimated. The $3,400 Year 1 cushion has different value to a buyer who’s stretched than to a buyer who isn’t.

Their rate forecast posture. If they believe rates are flat or rising for the next several years, the lower permanent rate looks better. If they think rates are likely to drop and they will refinance, the buydown looks better. The 10-year’s recent move suggests the latter is plausible.

The math is not the hard part. The judgment about which lever to pull is. That is the conversation worth having before lock day.

FAQ

Is the UWM 1-0 buydown actually free?

Free from the buyer’s perspective — they pay nothing out of pocket for the buydown. UWM funds it from their pricing margin. The trade-off is that the same buyer could lock a slightly lower permanent rate without the buydown. So while there is no upfront cost, there is an opportunity cost compared to the alternative permanent rate.

What is a 1-0 temporary buydown?

A 1-0 temporary buydown means the borrower’s effective interest rate is 1 percentage point lower than the note rate for the first 12 months. After that, it steps up to the full note rate for Year 2 through Year 30. The Year 1 subsidy is funded by a lump-sum credit at closing. That credit sits in an escrow account. It pays the lender the difference each month during the buydown period.

How much does the UWM 1-0 buydown save on a $600,000 loan?

On a $600,000 loan, the 1-point reduction is roughly $280 a month in lower principal and interest. That runs for 12 months, or about $3,400 in total first-year savings. The exact figure varies slightly based on the underlying note rate, but the order of magnitude holds across the typical conventional loan range.

What happens if the borrower refinances during Year 1?

If the loan is refinanced or paid off before the 12-month buydown period ends, any unused buydown funds in escrow are typically applied as a credit toward the new loan. Or returned to the borrower per the lender’s specific buydown agreement. The funds do not disappear, but the exact treatment depends on UWM’s program terms. Verify in writing before the loan closes.

When does the buydown beat the lower permanent rate?

The break-even sits around 3 years 7 months on a typical loan. Hold the loan less than that, and the buydown wins. Hold it longer, and the lower permanent rate wins. Many mortgages do not survive 3.5 years anyway. Between refinances and home sales, the average mortgage lifespan in the U.S. is 5 to 7 years. Many end sooner when rates drop.

The Bottom Line

UWM’s “Free” 1-0 buydown is a meaningfully good product right now. Not because it’s free in the absolute sense. Because the current rate environment makes the trade-off lean in its favor. The buyer gets real Year 1 relief. The cost is borne by the lender. The break-even falls well inside the window where most mortgages get refinanced anyway. For a buyer on the fence about whether the monthly payment works, this is the kind of product that moves the needle.

The trade-off against the slightly lower permanent rate is the conversation worth having before the buyer commits to either path. Run the numbers on their actual loan size. Ask the right questions about how long they plan to keep the loan. The right answer is almost always specific to the buyer, not the product.

If you have a client weighing affordability options, or deciding between a temporary buydown and a permanent rate, send them my way. Happy to walk through the math on their specific loan.

Don’t just take my word on the UWM 1-0 buydown

If you want a read on how I work with clients before sending one my way, here’s where past borrowers and partners have weighed in:

If you have a client weighing the UWM 1-0 buydown against a buy-down of the permanent rate, send them my way. We’ll run the actual numbers on their loan size, target rate, and realistic hold horizon.

Doctor loans let physicians, residents, and other eligible medical professionals finance up to 100% of a home's purchase price with no mortgage insurance.

TL;DR: Doctor loans let specific medical professionals borrow up to 100% of a home’s value with no mortgage insurance. The loans qualify through Fannie Mae and Freddie Mac. As a broker, I now have access to a doctor loans program that competes head-to-head with the big-bank versions. That means your client doesn’t have to use Chase or Bank of America to get the structure.

What are doctor loans, in plain English?

Your client tells you they’re a physician moving to Seattle for residency. Or a dentist buying their first home after years of student debt. Here’s what they need to hear: doctor loans are designed for them. They don’t punish them for the way medical careers actually work. People sometimes call them physician loans or medical professionals programs. They let eligible borrowers finance up to 100% of the purchase price with no mortgage insurance. They also treat deferred student loans differently than a conventional loan. And they let future income from a signed employment contract count for qualifying.

For years, the big retail banks owned these conforming Fannie Mae and Freddie Mac-eligible programs. Chase, BofA, Wells, a few regionals. The pitch was always the same. “Open a checking account with us and we’ll do your mortgage.” That worked when there was no alternative. Now there is.

Who qualifies for doctor loans?

The eligible degree list matters. Clients (and frankly some agents) assume “doctor loans” means anything with “Dr.” in front of the borrower’s name. They don’t. Specifically, the program I have access to qualifies these designations:

Doctor of Medicine (MD)

Doctor of Osteopathy (DO)

Doctor of Dental Surgery (DDS)

Doctor of Dental Medicine (DMD)

Doctor of Pharmacy (PharmD)

Doctor of Veterinary Medicine (DVM or VMD)

Doctor of Podiatric Medicine (DPM)

Certified Registered Nurse Anesthetist (CRNA)

Medical residents and fellows holding one of the above degrees

Borrowers need an active employment contract in their field, or documented offer acceptance. They also need to practice without supervision. Residents and fellows are the exception. Non-occupant co-borrowers work too. However, their income can’t be more than 50% of total qualifying income.

What’s not on the list trips agents up every time. Chiropractors. Registered nurses. Physician assistants. Nurse practitioners (unless they’re CRNAs). Psychologists, optometrists, audiologists, dental hygienists. If your client falls in that gap, they’re a conventional or FHA borrower. Not a doctor-loan borrower. Worth knowing before you write the offer.

Doctor loans by the numbers: LTV, FICO, and DTI

For a primary residence purchase or rate-and-term refinance, one-unit:

95% LTV up to $2,000,000 with a 680 FICO

100% LTV up to $1,500,000 with a 680 FICO

100% LTV up to $2,000,000 with a 720 FICO

Maximum DTI is 50% when the LTV is 95% or below. It’s 45% when LTV is between 90.01% and 100%. The program offers 15, 20, 25, or 30-year fixed terms. ARMs come in 5/6, 7/6, and 10/6 flavors. However, temporary rate buydowns aren’t eligible. Flag that for your client if their mom-and-dad-funded buydown was the plan.

Doctor loans vs. PMI: why no mortgage insurance matters

On a $1,000,000 loan at 95% LTV, monthly mortgage insurance on a conventional loan can run $300 to $600 a month. The exact number depends on the borrower’s credit and the MI company. That’s $3,600 to $7,200 a year your client throws away. The payment builds zero equity. It never goes to interest. It never reaches their tax accountant in any useful way. Doctor loans remove it entirely.

So when an agent tells me “the rate looks half a point higher than the conventional quote” — yes, sometimes it is. However, run the all-in payment with MI on the conventional. Doctor loans often win by $200 to $400 a month. Even with a slightly higher note rate. That’s the comparison your client should be looking at, not the rate alone.

Running the all-in payment with mortgage insurance on a conventional loan often shows doctor loans winning by $200–$400 a month — even with a slightly higher note rate.

Student loans: what gets excluded from DTI

This is the part that keeps doctors from qualifying anywhere else. For example: a new attending pulling $280,000 a year still has $400,000 in student loans in deferment. That normally kills mortgage qualification. A conventional underwriter wants to count 1% of the balance as a monthly payment. That’s $4,000 against the DTI right out of the gate.

Doctor loans exclude student loan payments from DTI when both of these are true. The borrower is currently in residency or a medical clinical fellowship. AND they’re qualifying based on the income they’re receiving during that residency or fellowship. Outside that lane — once they’re an attending, or qualifying on contract income that hasn’t started — the loan payment counts. But with flexibility on how:

If the credit report shows a real monthly payment, the underwriter uses that number

If the credit report shows $0 or no payment, the underwriter has options: a documented Income-Driven Repayment (IDR) amount, 1% of the balance for deferred or forbearance loans, or a fully amortizing payment using the actual repayment terms

The 1% rule sounds harsh. But it’s still better than what some lenders use. Those lenders apply the fully amortizing payment regardless of the actual situation.

Future income: signing a contract before the start date

Match Day is March 20th this year. New residents get told what city and what hospital. They sign a contract. They need housing — often before their first paycheck hits. Fortunately, doctor loans handle this with a projected income provision. A fully executed employment contract or offer letter qualifies the borrower. The start date can sit up to 150 days after the note date. For agents working with residents matching into UW Medicine, Seattle Children’s, Swedish, or Virginia Mason, this is the loan that turns “I can’t buy yet” into “let’s look at West Seattle and Beacon Hill this weekend.”

The contract has to spell out the position, start date, and salary. The only allowed contingencies are receipt of the medical license and normal administrative items. Background checks. Drug testing. Fingerprinting. The borrower also needs reserves to cover an extra month of PITIA (principal, interest, taxes, insurance, assessments) for every month between the first payment due date and the day employment starts.

Practical translation for agents: your client is house-hunting in February and starts work July 1st. This is the loan that lets them close in May. Build that into your timeline conversations.

Doctor loans accept a fully executed employment contract for qualifying, with a start date up to 150 days after the note date — built for Match Day timelines.

Reserves and gift funds

Reserves scale with loan size and LTV:

Loans $100,000 to $1,500,000 at LTV under 95%: 0 months reserves

Loans $1,500,001 to $2,000,000 at LTV under 95%: 3 months

Loans $100,000 to $1,500,000 at LTV over 95%: 3 months

Loans $1,500,001 to $2,000,000 at LTV over 95%: 6 months

Gift funds work, and they count toward reserves. That’s a meaningful difference from a lot of conventional loan programs. Documentation is light. One month of bank statements for refinances. Two months for purchases.

The Match Day window: an agent’s calendar reminder

Match Day is when fourth-year medical students find out which hospital they’ll do residency at. They learn where they’re moving. Most institutions send new residents a welcome packet with information about the area. Many of those packets include preferred lender and realtor contacts. So if you’re an agent in a market with a major teaching hospital, March is when you should be making sure you’re on that list. I work with brokers and agents who get added to those packets every year. Doctor loans are part of why that referral chain works.

For Puget Sound agents specifically: the Match Day window catches residents heading to UW Medicine in West Seattle’s broader catchment, Virginia Mason, Harborview, and the Swedish system across Seattle and Bellevue. Burien, Tukwila, and Renton tend to attract the dual-career resident households where one spouse commutes north for work — keep those neighborhoods on the showings list.

Doctor loans FAQ

Can doctor loans be used for a second home or investment property?

No. This program covers primary residence only — purchase or rate-and-term refinance. If your client wants to keep their current home and buy a new one, the new home has to be their primary. For investment property financing, they’d need a different product.

Do residents and fellows really qualify, or is it just for attendings?

Residents and fellows holding an MD, DO, DDS, DMD, PharmD, DVM, VMD, DPM, or CRNA degree qualify. The program treats them well. Their student loans drop out of DTI when the qualifying income is the residency or fellowship income. Projected income from a signed contract works if the start date sits within 150 days of the note date.

What’s the minimum credit score and loan amount for doctor loans?

The minimum FICO is 680. Minimum loan amount is $100,000 for fixed-rate products and $350,000 for ARMs. Maximum loan amount is $2,000,000.

How is this different from the doctor loan at a big bank?

The structure is similar. Most banks offer 100% LTV no-MI for medical professionals. However, the differences show up in pricing and the fine print. Some banks tack on a “you have to be our depository client” requirement. They also cross-sell aggressively. As a broker, I shop the loan rather than tying it to a deposit relationship. That usually means a more competitive rate. And a lender who isn’t trying to sell your client a wealth management package on the side.

Do doctor loans work for a borrower with a recent credit event?

The program requires four years since a major credit event or notice of default. Mortgage and rent history needs to be clean — zero 30-day lates in the past 12 months. If your client had something happen during med school or residency that’s still on their report, run the dates with me before you assume they’re disqualified.

Don’t just take my word on doctor loans

If you want a read on how I work with clients before sending one my way, here’s where past borrowers and partners have weighed in:

If you have a client matching at a Colorado or Washington hospital this Match Day cycle, or an attending who’s been told they need to put 20% down to avoid PMI — send them my way. Doctor loans are no longer a big-bank-only product.

Program details, guidelines, and pricing accurate as of April 30, 2026, and subject to change without notice. Loan approval is subject to underwriter review, credit qualification, and program eligibility at the time of application. Please contact me directly to confirm current program availability and verify that the terms outlined above are still in effect for your client’s specific situation.

A virtual mortgage closing lets everyone on the loan sign electronically from wherever they happen to be. The borrower, the co-buyer, the co-signer — each one joins a short video call with a remote notary, on their own schedule. Most lenders still won’t do this. Instead, they make every party show up in person at a title company on a specific day, at a specific time. However, United Wholesale Mortgage is one of the lenders that does offer virtual mortgage closing, in both Washington state and Colorado. I had a recent file with two co-buyers and two co-signers spread across multiple time zones, and what would have been a week of scheduling chaos turned into a non-event.

A virtual mortgage closing turns a beach chair into a closing table. Each signer logs in from wherever they are.

What a Virtual Mortgage Closing Actually Is

A virtual mortgage closing replaces the in-person signing room with a secure video call. Instead of driving to a title company, you log in from your laptop or phone. Specifically, the notarization happens through Remote Online Notarization, or RON. A licensed notary checks your ID over video and notarizes your signatures digitally. Subsequently, the closing team countersigns, the county records the deed, and the lender funds the loan. So legally, the transaction matches an in-person closing in every state that permits RON.

Overall, the difference is the friction. Nobody drives across town. Nobody rearranges the day. Consequently, the whole closing becomes a thirty-minute video session, and the bottleneck shifts from “get everyone in the same room” to “find a half-hour that works.”

Sign from the sidelines. Every party on the loan can join from anywhere on their own schedule.

Why Most Lenders Still Make Everyone Show Up in Person

RON has been legal in most states for years. Both Washington state and Colorado permit RON for mortgage closings, but lender adoption stays uneven. Specifically, building the technology takes real engineering work: secure ID verification, audio and video recording, integration with title companies and county recorders. Therefore, plenty of mid-sized lenders just haven’t built it. And some retail banks and credit unions still default to in-person closings because their compliance teams prefer that posture, full stop.

So if your client lands at a lender that doesn’t offer it, every signer has to physically appear at a title company. The slot is fixed: a specific date, a specific time. In theory that’s tolerable. In practice it’s the part of the deal where things break.

What Most People Don’t Realize: A Co-Signer Is a Co-Buyer

Here’s a misconception that bites a lot of buyers. When someone co-signs on a mortgage, they’re not just lending a credit score. Maybe a parent helps a kid qualify. Or a sibling lends their income. Or a friend bridges a credit gap. Whatever the situation, the co-signer signs the note. They’re on the loan. So they have to show up to the closing the same way the primary borrower does.

For example, take a parent in Spokane helping their daughter close on a house in Denver. Traditionally that meant flying out for a thirty-minute appointment. A co-signer who travels for work had to reschedule the trip. Likewise, someone already feeling like they’re doing the buyer a favor saw the in-person requirement as punishment for being generous. The friction isn’t theoretical. It lands hardest on the people doing the most help.

When a co-signer can’t physically travel, a virtual mortgage closing keeps the deal on schedule.

How a Virtual Mortgage Closing Solves the Logistics Problem

Once everyone on the loan can sign remotely, location stops mattering. First, each signer gets a link. Next, they join a short video session with the notary at a time that works. They walk through the documents on screen, then sign. The whole thing usually takes about an hour per signer, often less. Some sign from a kitchen table. Others sign on a lunch break. Three signers can do it in three different time zones on the same day, and nobody has to coordinate calendars beyond their own.

Finally, the deal closes on schedule. Nobody flies in. Nobody takes a half-day off work. The buyer gets the keys.

A Recent Example: Two Co-Buyers, Two Co-Signers, Four Schedules

A recent file of mine had two co-buyers and two co-signers, four signers total. Each one lived in a different city. Each one kept a different schedule. Under the old model, this kind of deal drags closing out by a week while everyone tries to find a mutual two-hour window. With UWM’s virtual mortgage closing, though, each of the four signed at their own convenience. The whole signing wrapped inside a single business day. All four sat in different time zones; the property was here in South King County.

Overall, the narrative for my client flipped completely. What used to feel like extreme inconvenience for the people doing them a favor became extreme convenience instead. That’s not a small thing. Treat co-signers and co-buyers well at closing, and they say yes the next time a family member asks for help.

On the other side: a remote notary runs the closing for two borrowers over video.

What This Means for Your Next Deal

If you’re a real estate agent and your buyer needs a co-signer to qualify, the lender choice matters more than people realize. By contrast, a lender without virtual mortgage closing can turn a clean qualification into a logistics scramble on day 28 of a 30-day close. So ask early, before the buyer commits, whether the lender supports it. The question is simple: “Do you offer Remote Online Notarization for every party on the loan, in this state, on this product?” The answer should come back yes, no, or a quick check. Never a long story. For West Seattle, Vashon Island, and Bainbridge Island agents in particular, ferry schedules and Friday traffic can turn a one-hour closing into a half-day operation. Virtual closing removes that variable entirely.

Is a virtual mortgage closing legally the same as an in-person one?

Yes. Indeed, RON produces a legally binding mortgage in every state that permits it, including Washington and Colorado. The county records the deed the same way. The lender funds the loan the same way. Signing and notarization just happen over secure video instead of across a table.

Is a co-signer the same as a co-buyer on a mortgage?

For mortgage purposes, yes. A co-signer signs the note and joins the loan, so they count as a co-buyer in everything that matters at closing. They sign the same documents the primary borrower signs. They attend the closing the same way, virtually or in person.

Why don’t more lenders offer virtual mortgage closing?

Two reasons. First, the technology stack takes real engineering that smaller lenders haven’t built: identity verification, secure video, integration with title companies and county recorders. Second, some lenders’ compliance teams still prefer in-person closings as their default, even where RON is fully legal. Notably, UWM ranks among the few wholesale lenders that have rolled out RON broadly.

Can a virtual mortgage closing work if signers are in different states?

Yes, in most cases. Specifically, RON laws apply to the notary’s location, not the signer’s. So as long as the notary holds a license in a state that permits RON for mortgage closings, signers can join from anywhere with a stable internet connection. For deals with co-buyers and co-signers spread across multiple states, that’s the whole point.

Don’t just take my word on virtual closings

If you want a read on how I work with clients before sending one my way, here’s where past borrowers and partners have weighed in:

If you have a client who needs a co-signer or co-buyer to qualify and you want to know whether their lender will make closing day painless or painful, send them my way. We do virtual closings as a default, not an exception.

Home Loan Originators Christopher Gibson & Brandon Gibson at C2 Financial Corporation are your online resource for personalized mortgage solutions, fast customized quotes, great rates, & service with integrity. Licensed to originate loans in all of Colorado. We primarily utilize United Wholesale Mortgage to offer the highest quality service and technology to make the mortgage process as easy on our clients as possible. We reduce our compensation to attempt to secure the lowest rates and costs possible for our clients, as well and we want to provide the best service AND the best rates. Christopher & Brandon Gibson are brothers and Colorado natives. They began in the mortgage industry in 2019. Serving mostly friends and family, client satisfaction and referral business is their focus.

Disclosure

This licensee is performing acts for which a real estate license is required. C2 Financial Corporation is licensed by the Colorado Department of Real Estate, NMLS # 135622 NMLS# 1910935. Loan approval is not guaranteed and is subject to lender review of information. All loan approvals are conditional and all conditions must be met by borrower. Loan is only approved when lender has issued approval in writing and is subject to the Lender conditions. Specified rates may not be available for all. Rates subject to change with market conditions. C2 Financial Corporation is an Equal Opportunity Mortgage Broker/Lender. The services referred to herein are not available to persons located outside the state of Colorado.www.GibsonHomeLoans.com | Chris Gibson | (720) 394-8861 | C@ChrisRayGibson.com | Brandon Gibson | (303) 332-5523 | B@BrandonPGibson.com

Denver Realtor Reviews: Colorado Real Estate Market Statistics for December 2021

Real Estate Market Statistics for the metro Denver area, Colorado Springs Pikes Peak region, and Northern Colorado.

Metro Denver Colorado Real Estate Market Statistics as of December 2021 Denver metro is generally composed of Adams, Arapahoe, Broomfield, Denver, Douglas, Elbert, and Jefferson Counties. Metro Denver in Colorado saw a 62.6% decrease in the real estate inventory, which is the number of homes available for sale. Additionally, the Denver front range which includes Denver, Aurora, Lakewood, Thornton, Arvada, Westminster, Centennial, and Highlands Ranch as the largest cities in the area saw a 12.0% decrease in new listings and a 9.8% decrease in closed home sales. The median home price in Denver metro increased by 19.4% from $452,001 to $539,748.

Southern Front Range Colorado Real Estate Market Statistics as of December 2021

Colorado Springs is generally composed of El Paso County and Teller Counties. The Pikes Peak region in Colorado saw a 9.2% decrease in the real estate inventory, which is the number of homes available for sale. Additionally, the southern front range around Colorado Springs, which includes Colorado Springs, Monument, Falcon, Fountain, Manitou Springs, and Woodland Park saw a 4.9% increase in new listings and a 21.3% increase in closed home sales. The median home price in Colorado Springs metro increased by 20.0% from $400,000 to $480,000.

Northern Colorado Real Estate Market Statistics as of December 2021

Northern Colorado is generally composed of Boulder, Larimer, Logan, Moran, and Weld Counties. The Northern Front Range region in Colorado saw a 67.2% decrease in the real estate inventory, which is the number of homes available for sale. Additionally, the northern front range area that includes Boulder, Broomfield, Fort Collins, Greeley, Longmont, and Loveland saw an 11.4% decrease in new listings and a 10.7% decrease in closed home sales. The median home price in northern Colorado increased by 16.5% from $420,000 to $489,265.

When looking into mortgage options, it is important to research the mortgage rate trend and review what mortgage experts predict. As home loan originators, we work hard to stay up to date on the mortgage rate trend for our clients. Here is the latest mortgage rate trend forecast for this week.

Mortgage Experts

Mortgage experts mostly think rates will rise in the coming week (Jan. 27 – Feb. 2). In response to Bankrate’s weekly poll, 80% said rates are headed higher. Meanwhile, 10% said they would remain the same and another 10% predicted they would fall.

Based on the mortgage rate trend, it might be a good time to consider refinancing your current mortgage. Refinancing is the process of paying off your existing mortgage with a new mortgage. Typically, you refinance your mortgage to reduce your interest rate and monthly payment or change the length (or term) of your mortgage. You may also refinance to take cash out from your home’s equity.

Your Rate Options

A great way to begin the process of refinancing is to look at your rate options. We would love to help you out. Click the link below to determine what rate options are available to you: https://gibsonratecheck.com

Refinance Process

Are you curious about how the refinance process works? Here’s how our home refinance process works:

Receive options based on your unique criteria and scenario

Compare mortgage interest rates and terms

Choose the offer that best fits your needs

We Want To Help

As licensed loan originators serving all of Colorado, we primarily utilize United Wholesale Mortgage to offer the highest quality service and technology to make the mortgage process as easy on our clients as possible. Our top priority is to provide the best service AND the best rates.

As brothers and Colorado natives, we serve mostly friends and family. Client satisfaction and referral business is our focus.