Evaluating the HOA on a Condominium for an FHA Reverse Mortgage

Evaluating the HOA on a Condominium for an FHA Reverse Mortgage

Start here before ordering any condo questionnaires.

This guide is for real-estate agents, financial advisors, and savvy homeowners evaluating the HOA on a condominium for an FHA reverse mortgage. Use it to avoid expensive surprises and loan denial.

TL;DR – Quick Wins When Evaluating the HOA on a Condominium for an FHA Reverse Mortgage

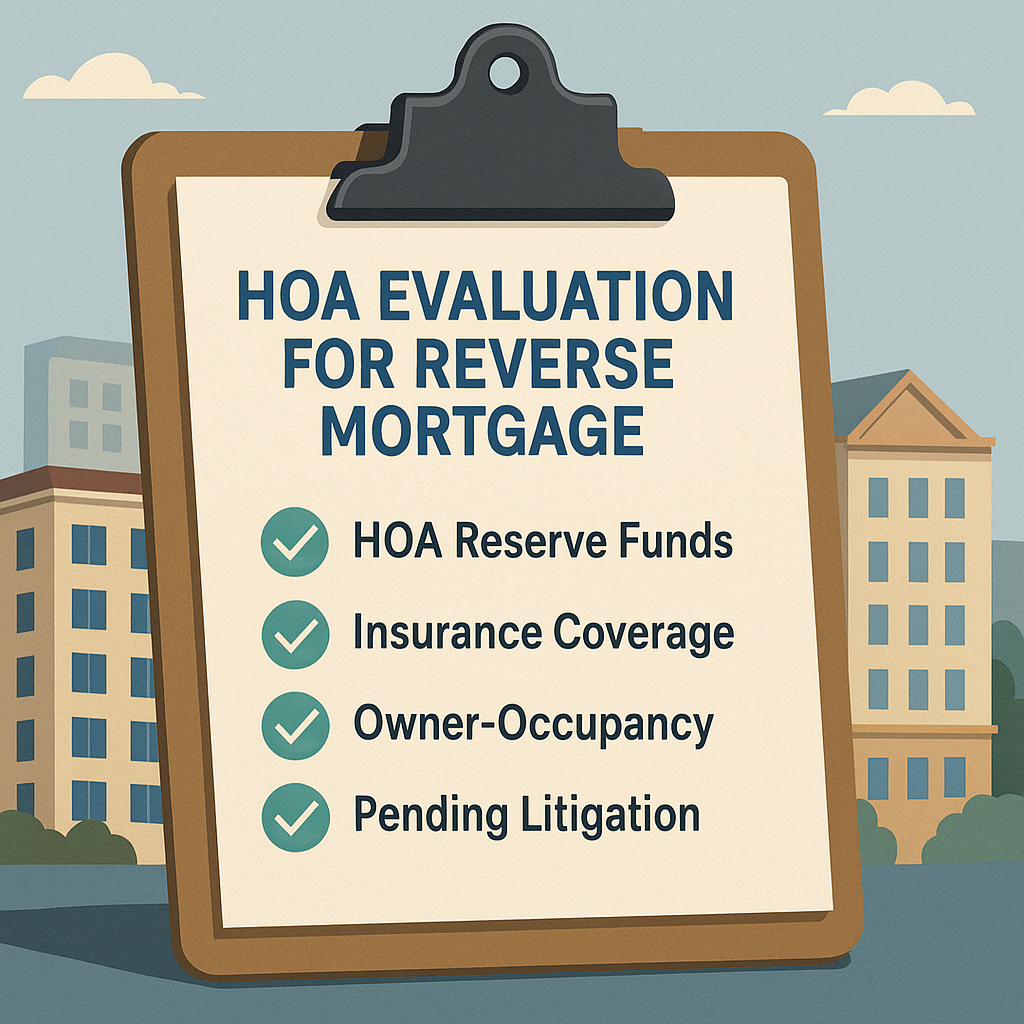

Verify ≥ 50 % owner-occupancy and < 15 % delinquencies.

Scan the HUD-9991 form before paying for a condo cert.

Check the master policy for 100 % replacement cost and deductibles under $10 k.

Email the 10 questions in Step 6 first—save time and money.

Step 1 – FHA Spot-Approval Basics for Evaluating the HOA on a Condominium

Project complete—no active construction.

≥ 5 units, ≥ 50 % owner-occupied.

≤ 10 % FHA concentration (max 2 units if < 10 total).

No unresolved litigation or financial distress.

Step 2 – HOA Financial Health When Evaluating the HOA on a Condo for an FHA Reverse Mortgage

≥ 10 % of budget to reserves or a reserve study < 24 months old.

Delinquencies below 15 %.

Operating and reserve funds in separate accounts.

Owner-occupancy, reserves, and delinquency rates drive FHA approval odds.

Step 3 – Insurance Traps When Evaluating the HOA on a Condominium for an FHA Reverse Mortgage

100 % replacement-cost hazard coverage.

≥ $1 M liability.

Fidelity bond if 20+ units or >$50 k in funds.

Flood insurance if required by FEMA.

Watch out: massive deductibles on roofs or “walls-in” exclusions.

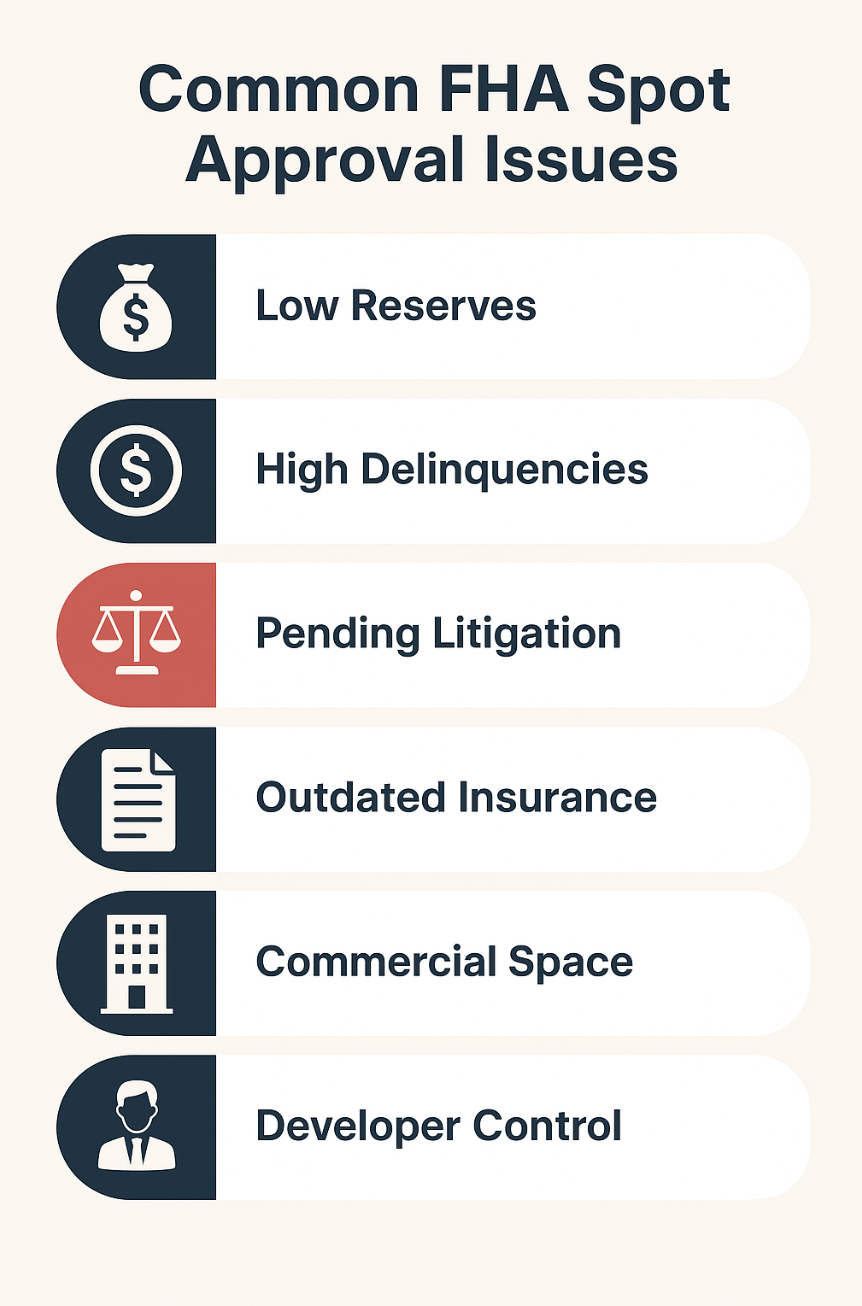

Step 4 – Deal-Killers That Stop an FHA Reverse Mortgage on a Condo

Reserves underfunded or no recent study.

Delinquencies > 15 %.

Pending structural litigation.

Commercial space > 35 %.

These issues derail FHA spot approval immediately.

Step 5 – General HOA Health Tips for an FHA Reverse Mortgage

Reserve study funded ≥ 70 %.

Budgets & meeting minutes readily available.

Common areas kept in good repair.

Step 6 – Pre-Screen Email While Evaluating the HOA on a Condominium

Copy/paste and send before paying for a condo cert:

Subject: A couple of questions before I request a questionnaire

To whom it may concern,

Questionnaires have become very expensive. Could you please help me determine the following before I spend a lot of $ on a questionnaire.

Is the current owner-occupancy percentage greater than 50%?

Are more than 15% of units 60+ days delinquent?

Does any owner/entity own >10 % of units?

Could you send me the master insurance policy?

Does the HOA perform any short-term rental property management activities?

Is there any structural deferred maintenace that would be identified in a questionnaire?

Are there any current special assessments?

Is there any pending litigation?

Is the HOA developer controlled? Are there any portions of the project still under construction?

Do you know if there is commercial space and if so, is it more than 35% of the total square footage?

Frequently Asked Questions

What makes a condo ineligible for an FHA loan or reverse mortgage?

High delinquencies, low reserves, litigation, or missing insurance.

Agents, advisors, and informed homeowners rely on this checklist.

About the Author

Christopher Gibson is a mortgage loan officer licensed in CO, FL, MI, TX, GA, and WA, and a former real-estate agent. He specializes in FHA reverse mortgages and condo lending strategies.

Down payment assistance programs continue to be valuable resource for homebuyers across the country. To help our real estate partners grow their business and better serve borrowers, we offer an exclusive 0% Down Purchase program through UWM. Simply put, qualified borrowers receive a 3% down payment assistance loan, up to $15,000, from UWM. This allows our partners to help more buyers get into a home right now with no down payment.

Here’s how it works:

First lien mortgage meets LTV requirements

UWM provides a second lien mortgage for 3% of the purchase price, up to $15,000

Second lien has no monthly payment requirement and no interest

Second lien balance is due when the first lien loan is refinanced or paid off, whichever comes first

Payments on the second lien can be made throughout the loan term, but are not required

How borrowers can qualify:

Borrowers must be at or below 80% of the Area Median Income (AMI) for the address of the property they are buying and meet Home Possible® guideline requirements

For very-low income borrowers whose qualifying income is at or below 50% AMI (VLIP borrowers), they will receive a $2,500 credit as part of the 3% assistance

This credit does not need to be repaid by the borrower and lowers their debt obligation from the second lien

620+ FICO and LTV must be equal to or greater than 95% LTV, up to 97%

—OR—

At least one borrower must be a first-time homebuyer and meet HomeOne® and UWM’s guideline requirements

First-time homebuyer is defined as someone who has not had ownership interest in a home in the last 3 years

700 FICO and LTV must be greater than 95%, up to 97%

Information subject to change. Certain restrictions apply. Subject to approval of borrower and investor guideline requirements. Down payment is provided as a 2nd lien against the subject property. 2nd lien bears a 0% interest rate and cannot exceed a $15,000 loan amount. 2nd lien has no minimum monthly payment requirements, a term of 360 months and is fully due as a balloon payment upon the occurrence of either a refinance of the 1st lien, payoff of the 1st lien or the final payment of the amortization schedule of the 1st lien. Borrower must qualify based on Home Possible® or HomeOne® guidelines. Some exclusions may apply.

The principal, interest, and MI payment of a $350,000 30-year Fixed-Rate Loan at 6.75% and 97% loan-to-value (LTV) is $2270.09. The Annual Percentage Rate (APR) is 6.949% with estimated finance charges of $6,500. The principal and interest payments, which will continue for 360 months until paid in full, do not include taxes and home insurance premium, which will result in a higher actual monthly payment. Rates current as of 5/20/24. Subject to borrower approval. Some exclusions may apply.

Understanding Modular and Manufactured Homes: Financing Challenges and Opportunities

The Distinct Differences Between Modular and Manufactured Homes

Modular homes are constructed in sections at a factory and assembled on-site on a permanent foundation, adhering to local and state building codes. Manufactured homes, built entirely in a factory under the Federal HUD building code, can be placed on permanent or non-permanent foundations. Telling the difference between a manufactured home and a modular home by just looking at them can be challenging, especially since both types of homes have evolved in terms of design and quality. However, there are a few general indicators that might help distinguish between the two:

Foundation and Undercarriage:

Manufactured Homes: Typically, they are built on a non-removable steel chassis and may have visible undercarriage or a skirting area covering the space between the home and the ground.

Modular Homes: These are usually set on a traditional concrete foundation that’s similar to site-built homes and don’t have a visible steel chassis or undercarriage.

Appearance and Design:

Manufactured Homes: Often come in single or double-wide configurations and might have a more rectangular shape. The roof pitch tends to be lower, and the exterior design may be more simplistic.

Modular Homes: They can be virtually indistinguishable from traditional site-built homes. They offer more variety in design, including multi-story options, higher roof pitches, and diverse architectural styles.

Transportation:

Manufactured Homes: These homes are often seen transported in whole sections on roads, with transportation tags visible.

Modular Homes: Transported in sections or modules, but once assembled on their foundation, they don’t resemble a structure that has been transported.

HUD Tag vs. Local Building Codes:

Manufactured Homes: Should have a HUD tag or certification label, indicating compliance with federal standards.

Modular Homes: They don’t have HUD tags. Instead, they are built to comply with local and state building codes, and documentation or certification might be available through local building permits and inspections.

Exterior Utilities and Connections:

Manufactured Homes: Utility connections might be more visible, similar to a mobile home.

Modular Homes: Utilities are typically connected in a way that’s similar to site-built homes, often less visible.

Despite these general guidelines, it’s important to note that the lines between manufactured and modular homes can blur, especially with advancements in factory-built housing. Sometimes, the only sure way to differentiate is through looking at the documentation or building permits of the home.

Telling the difference between a manufactured home and a modular home by just looking at them can be challenging, especially since both types of homes have evolved in terms of design and quality. However, there are a few general indicators that might help distinguish between the two:

Foundation and Undercarriage:

Manufactured Homes: Typically, they are built on a non-removable steel chassis and may have visible undercarriage or a skirting area covering the space between the home and the ground. Modular Homes: These are usually set on a traditional concrete foundation that’s similar to site-built homes and don’t have a visible steel chassis or undercarriage. Appearance and Design:

Manufactured Homes: Often come in single or double-wide configurations and might have a more rectangular shape. The roof pitch tends to be lower, and the exterior design may be more simplistic. Modular Homes: They can be virtually indistinguishable from traditional site-built homes. They offer more variety in design, including multi-story options, higher roof pitches, and diverse architectural styles.

Transportation:

Manufactured Homes: These homes are often seen transported in whole sections on roads, with transportation tags visible. Modular Homes: Transported in sections or modules, but once assembled on their foundation, they don’t resemble a structure that has been transported.

HUD Tag vs. Local Building Codes:

Manufactured Homes: Should have a HUD tag or certification label, indicating compliance with federal standards. Modular Homes: They don’t have HUD tags. Instead, they are built to comply with local and state building codes, and documentation or certification might be available through local building permits and inspections.

Exterior Utilities and Connections:

Manufactured Homes: Utility connections might be more visible, similar to a mobile home. Modular Homes: Utilities are typically connected in a way that’s similar to site-built homes, often less visible.

Despite these general guidelines, it’s important to note that the lines between manufactured and modular homes can blur, especially with advancements in factory-built housing. Sometimes, the only sure way to differentiate is through looking at the documentation or building permits of the home.

Navigating Financing Challenges

Modular homes may face issues such as appraisal difficulties and lender misconceptions, requiring construction loans for both land and home construction. Manufactured homes encounter challenges like strict HUD code compliance, titling issues, and higher interest rates and down payments.

Fannie Mae, Freddie Mac Requirements, and HUD Guidelines for Manufactured Homes

Financing for manufactured homes through Fannie Mae and Freddie Mac involves specific criteria:

Size Requirements: The home must be at least 400 square feet and 12 feet wide. Construction and Installation: Built to HUD Code, on a permanent chassis, and installed on a permanent foundation system. Titling and Land Lease Limitations: Must be titled as real estate. Fannie Mae generally does not purchase manufactured housing loans if the home is on a leased lot or in a leasehold community. The land must typically be owned outright by the homeowner, which can limit financing options for homes not owned with the land. HUD Tag Requirement: The HUD tag, affixed to each section of a manufactured home, certifies compliance with HUD standards, containing information such as the serial number and date of manufacture.

Movement of manufactured homes

There are specific rules and considerations regarding the movement of manufactured homes when using a conforming loan, particularly those backed by Fannie Mae or Freddie Mac. Here’s a summary of the key points:

Movement from the Original Site:

Manufactured homes are expected to be transported directly from the manufacturer to the final site. If a manufactured home has been moved from its original site (where it was first installed), it typically becomes ineligible for a conforming loan. This policy is in place because moving a manufactured home can potentially compromise its structural integrity and may also indicate it was previously used, which can affect its eligibility.

One-Time Move Rule:

The general rule for conforming loans is that the manufactured home should only be moved once – from the factory to the lot where it is to be permanently located. Any subsequent moves after the initial placement can disqualify the home from most conventional financing options.

Documentation and Certification:

Lenders may require specific documentation to prove that the home has not been moved from its original installation site. This might include transport records, installation permits, or other forms of certification.

Financing Limitations for Manufactured Homes vs. Site-Built Homes

Maximum LTV for First-Time Home Buyers: For manufactured homes, the maximum loan-to-value (LTV) ratio is capped at 95% for first-time home buyers, compared to 97% for site-built homes under Fannie Mae’s standard transactions.

Condominium Communities and Manufactured Homes

In condominium communities, manufactured homes may not need to be owned with the land. However, this is an exception and not the norm for financing manufactured homes, as Fannie Mae typically requires the land to be owned by the homeowner. For these communities, both the land and dwelling, must be subject to the condo regime. PERS (Project Eligibility Review Service) approval is required for all condo, co-op, or PUD projects that consist of single-width manufactured homes and for some projects with multi-width manufactured homes.

Tiny Homes

Tiny homes are built to HUD standards. According to the U.S. Department of Housing and Urban Development (HUD), tiny homes that rest on a skid or foundation — or are over 400 square feet — now fall squarely under the HUD manufactured housing standards 1. HUD prohibits the sale and lease of homes that do not meet federal standards, and tiny home builders are now entering a new era of compliance. In order to be occupied, a tiny home must comply with the standards of, and be approved as one of the following types of structures: a HUD-Code manufactured home (MH), California Residential Code or California Building Code home, factory-built housing (FBH), recreational vehicle (RV), park trailer (PT) or camping cabin (CC). If a tiny home is not built according HUD standards, it will not qualify for a conforming mortgage, however being built according to HUD standards will not qualify a tiny home for a conforming mortgage in of itself.

Emerging Solutions and Developer Considerations

The landscape is evolving with a focus on sustainability, affordability, and technology. Developers should consider regional demand, mortgage rates, and material costs. Flexible floor plans, outdoor living spaces, and technology enhancements can improve appeal. Staying informed about trends and regulatory changes in the manufactured and tiny home sectors is crucial for navigating the financing landscape and capitalizing on market opportunities.

For those stepping into the realm of homeownership for the first time, weighing the options between FHA vs conventional loans is crucial. Let’s delve into the key distinctions and benefits of each loan category.

Federal Support for FHA Loans for Novice Homebuyers

FHA loans enjoy federal government support, unlike their conventional counterparts. This backing allows for more lenient criteria regarding down payments and credit scores for FHA loans. However, they come with higher associated fees and mortgage insurance costs.

Variations in Credit Scores for FHA and Conventional Loans for New Homebuyers

While FHA loans mandate a minimum credit score of 580 and a down payment as low as 3.5%, conventional loans generally ask for a credit score starting at 620 and a minimum down payment of 3%. Note that these requirements can vary with different lenders and are influenced by the borrower’s specific circumstances and prevailing market trends.

Differences in Mortgage Insurance for FHA and Conventional Loans for First-Time Buyers

FHA loans include both an upfront and a monthly mortgage insurance premium, typically 1.75%, potentially increasing the overall cost of the loan. In contrast, conventional loans require private mortgage insurance (PMI), payable either monthly or in a lump sum, and it may cease once the loan-to-value (LTV) ratio hits 78%.

Interest Rate Disparities Between Conventional and FHA Loans for New Homebuyers

FHA loans often feature lower interest rates compared to conventional loans, potentially making them more cost-effective over time. However, it’s worth noting that conventional loans have recently adjusted their rates for moderate-income, first-time buyers, thereby enhancing their competitiveness against FHA loans.

Loan Limit Variances Between FHA and Conventional Loans for First-Time Homebuyers

FHA loans are subject to lower borrowing limits, which might restrict purchasing higher-priced properties. On the other hand, conventional loans offer higher limits that vary regionally and adhere to Fannie Mae and Freddie Mac guidelines, the government-backed entities involved in mortgage trading.

Eligibility Criteria for Conventional and FHA Loans for Novice Homebuyers

FHA loans are generally more accessible, with less stringent requirements concerning debt-to-income ratios, income proof, and credit history. Conversely, conventional loans maintain more rigorous standards, potentially challenging for applicants with lower credit scores, higher debt ratios, or recent financial setbacks like bankruptcy or foreclosure.

Appraisal and Inspection Requirements for FHA vs. Conventional Loans for First-Time Buyers

FHA loans might be less appealing to sellers due to their stringent appraisal and inspection mandates, possibly hindering the closing process. In contrast, conventional loans often present fewer obstacles, potentially enhancing the buyer’s leverage in negotiations.

Additional Factors for FHA and Conventional Loans for New Homebuyers

It’s important to note that many condo developments might not qualify for FHA loans due to HOA certification requirements. Additionally, the minimum down payment for manufactured homes is 5%, which could make FHA loans a more attractive option for these property types.

In conclusion, the choice between an FHA and a conventional loan for first-time homebuyers hinges on individual financial situations, objectives, and preferences. It’s advisable to thoroughly assess the costs and advantages of each loan type before making a decision. Wishing you the best in your homebuying journey!

FHA vs Conventional: Detailed Loan Guide for Homebuyers

FHA vs Conventional Loans for First-Time Homebuyers

For first-time homebuyers, navigating between FHA and conventional loans can be complex. This guide delves into the specifics of each to inform your decision.

Property Condition Requirements: A Closer Look

FHA loans require properties to meet specific conditions related to safety and habitability, like addressing chipping paint, ensuring functioning kitchens and bathrooms, and fixing broken windows or water damage. Conventional loans, with less specific requirements, might require corrections for issues like peeling paint, roof damage, or deficiencies in mechanical systems if noted by an appraiser.

Non-Occupant Co-Borrowers: FHA vs Conventional Rules

FHA loans generally require non-occupant co-borrowers to be family members, with a maximum LTV of 96.5%. For conventional loans, the maximum LTV is 95% with co-borrowers on title, offering a slightly different approach in terms of flexibility and LTV limits.

Down Payment and Gift Funds: Understanding the Differences

The FHA requires a minimum 3.5% down payment, which must be from the borrower’s funds or a down payment assistance program. In contrast, conventional loans allow for the entire down payment to be gifted, providing more flexibility for first-time home buyers.

DTI and Housing Expense Ratios: FHA vs Conventional

FHA loans often allow higher DTI ratios, potentially as high as 57%, compared to a maximum of 49% for conventional loans. This difference can be crucial for borrowers balancing income and debt.

Cost Comparisons: FHA and Conventional Loans

FHA loans include a 1.75% upfront mortgage insurance fee, with ongoing insurance for loans with less than 10% down. Conventional loans, however, terminate mortgage insurance automatically when the LTV reaches 79%.

Interest Rates and Credit Scores: A Comparative Analysis

With FHA loans generally offering lower interest rates and being more accommodating of lower credit scores, they often present a more accessible option for first-time buyers, especially in high LTV scenarios.

Loan Limits: Understanding the Variations

FHA loan limits are set at 65% of conventional loan limits, affecting the maximum borrowing capacity. For example, if conventional loan limits are $766,550, the FHA limit would be around $498,257.

November 2023 Mortgage Trends: An Insight into Home Financing

As the year 2023 progresses, especially as of November, the mortgage industry has experienced significant shifts. These November 2023 mortgage trends have a profound impact on homebuyers, particularly those considering a substantial investment like a $400,000 loan.

25 Days Ago: Monthly payment was approximately $2,742.56.

5 Days Ago: Monthly payment was approximately $2,542.76.

Today: Monthly payment is approximately $2,490.51.

November 2023 Mortgage Rate Changes: A Closer Look

From 25 Days Ago to 5 Days Ago: Monthly payment decreased by approximately $199.80. From 5 Days Ago to Today: Monthly payment decreased by approximately $52.25.

Calculate your potential mortgage payments using our payment calculator.

Factors Influencing the November 2023 Mortgage Market

The recent decrease in the 10 Year Treasury Spread and 10-Year Close can be attributed to several strategic decisions and market responses. These include the Treasury Department’s issuance strategy and the Federal Reserve’s policy decisions…

Understanding the 2024 Colorado Conforming Loan Limits from FHFA

The Federal Housing Finance Agency (FHFA) plays a pivotal role in the U.S. housing market, particularly in setting the 2024 Colorado conforming loan limits. These limits are crucial as they dictate the maximum loan amounts for standard mortgages backed by government-sponsored enterprises like Fannie Mae and Freddie Mac. Learn more about Conforming Loan Limits from FHFA.

What are the 2024 Colorado Conforming Loan Limits from FHFA?

For 2024, the FHFA has set the conforming loan limit at $766,550, a 5.5% increase from 2023. This adjustment reflects changes in the average U.S. home price, allowing borrowers in areas like Colorado to access higher loan amounts under favorable terms. Start your mortgage application today.

High Balance Loans: A Closer Look

In high-cost areas, the conforming loan limits are stretched to accommodate the higher property values. For 2024, the high balance limit is set at $1,089,300. However, these loans often come with higher interest rates due to the increased lending risk. Get a home value estimate.

Metro Denver’s Unique Position

Metro Denver stands out with a conforming loan limit of $816,500 for 2024. Other high-cost counties in Colorado may experience even higher limits, reflecting the diverse real estate market within the state. Search homes for sale in Colorado.

Understanding Jumbo Loans

Loans exceeding the conforming limits are categorized as Jumbo Loans. These are significant for luxury properties or high-cost areas, requiring stringent borrowing criteria due to the absence of government backing. Use our payment calculator to explore options.

Act Now: Closing 2024 Loans in 2023

Interestingly, borrowers can close on these 2024 loan limits right now in 2023, offering a unique opportunity for those looking to invest in Colorado’s dynamic real estate market. Contact us for personalized assistance.

2024 Colorado Conforming Loan Limits Table

County Name

One-Unit Limit

Two-Unit Limit

Three-Unit Limit

Four-Unit Limit

ADAMS COUNTY

$816,500

$1,045,250

$1,263,500

$1,570,200

ALAMOSA COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

ARAPAHOE COUNTY

$816,500

$1,045,250

$1,263,500

$1,570,200

ARCHULETA COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

BACA COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

BENT COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

BOULDER COUNTY

$856,750

$1,096,800

$1,325,800

$1,647,650

BROOMFIELD COUNTY

$816,500

$1,045,250

$1,263,500

$1,570,200

CHAFFEE COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

CHEYENNE COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

CLEAR CREEK COUNTY

$816,500

$1,045,250

$1,263,500

$1,570,200

CONEJOS COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

COSTILLA COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

CROWLEY COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

CUSTER COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

DELTA COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

DENVER COUNTY

$816,500

$1,045,250

$1,263,500

$1,570,200

DOLORES COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

DOUGLAS COUNTY

$816,500

$1,045,250

$1,263,500

$1,570,200

EAGLE COUNTY

$1,149,825

$1,472,250

$1,779,525

$2,211,600

ELBERT COUNTY

$816,500

$1,045,250

$1,263,500

$1,570,200

EL PASO COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

FREMONT COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

GARFIELD COUNTY

$1,149,825

$1,472,250

$1,779,525

$2,211,600

GILPIN COUNTY

$816,500

$1,045,250

$1,263,500

$1,570,200

GRAND COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

GUNNISON COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

HINSDALE COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

HUERFANO COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

JACKSON COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

JEFFERSON COUNTY

$816,500

$1,045,250

$1,263,500

$1,570,200

KIOWA COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

KIT CARSON COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

LAKE COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

LA PLATA COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

LARIMER COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

LAS ANIMAS COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

LINCOLN COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

LOGAN COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

MESA COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

MINERAL COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

MOFFAT COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

MONTEZUMA COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

MONTROSE COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

MORGAN COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

OTERO COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

OURAY COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

PARK COUNTY

$816,500

$1,045,250

$1,263,500

$1,570,200

PHILLIPS COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

PITKIN COUNTY

$1,149,825

$1,472,250

$1,779,525

$2,211,600

PROWERS COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

PUEBLO COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

RIO BLANCO COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

RIO GRANDE COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

ROUTT COUNTY

$1,012,000

$1,295,550

$1,566,050

$1,946,200

SAGUACHE COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

SAN JUAN COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

SAN MIGUEL COUNTY

$994,750

$1,273,450

$1,539,350

$1,913,000

SEDGWICK COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

SUMMIT COUNTY

$1,006,250

$1,288,200

$1,557,150

$1,935,150

TELLER COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

WASHINGTON COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

WELD COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

YUMA COUNTY

$766,550

$981,500

$1,186,350

$1,474,400

How is high cost determined for 2024 Colorado Conforming Loan Limits

The Housing and Economic Recovery Act of 2008 (HERA) requires annual adjustments to the Federal Housing Finance Agency’s (FHFA) conforming loan limit (CLL) to reflect changes in the national average home price. Using the House Price Index (HPI), the FHFA’s 2024 CLL increase is calculated at 5.56%. HERA also establishes high-cost area limits, set at a percentage above the baseline. For 2024, the maximum high-cost area limit is $1,149,825, 150% of the baseline $766,550.

Conclusion

Understanding the 2024 Colorado FHFA Conforming Loan Limits is vital for anyone looking to navigate the real estate market, whether it’s opting for a standard, high balance, or jumbo loan.

Market Chaffee and Lake Counties: October 2023 Overview

Market Chaffee and Lake Counties: An Insightful October 2023 Overview

Introduction

Nestled in the heart of Colorado, Chaffee and Lake Counties offer a blend of natural splendor and real estate opportunity that’s hard to find elsewhere. This October 2023 market report provides an in-depth look at the core market statistics that paint a picture of current trends, aiding buyers, sellers, and enthusiasts alike to make informed decisions.

Chaffee County: A Blend of Nature and Community

Chaffee County, with its diverse landscape, is characterized by the Arkansas River’s winding paths and the towering peaks of the Sawatch Range. Salida, the largest city, sits approximately 7,083 feet above sea level…

Lake County: High-altitude Living with a Historical Twist

Adjacent Lake County is home to Leadville, the highest incorporated city in North America, perched at an elevation of about 10,152 feet…

Median Close Price

In October 2023, the median close price was $654,500, which is an increase from $634,000 in September 2023 and a significant rise from $569,000 in October 2022. This upward trend suggests a growing market, potentially favoring sellers with higher property values.

Active Listings

The number of active listings stood at 52 in October 2023, down from 45 in September 2023 but slightly up from 49 in October 2022. The small increase in listings year over year could indicate a more favorable environment for buyers.

Sales Numbers

The sales numbers for October 2023 were at 248, a decrease compared to 271 sales in September 2023 but an increase from 207 sales in October 2022. This points to a still-active market with more transactions occurring than the previous year.

Close Price to Original Price Ratio

As for the close price to the original price ratio, there was a slight decrease to 95% in October 2023 from 96.1% in September 2023, but an increase from 94.6% in October 2022. This could indicate that while sellers are getting closer to their asking price, buyers have had slightly more negotiating power than in the previous month.

Your Trusted Advisor

For personalized advice and insights, reach out to Christopher Gibson, a seasoned expert in the market Chaffee and Lake Counties…

Park, Gilpin, Clear Creek Real Estate Market Report October 2023

Park, Gilpin, Clear Creek Real Estate Market Insights – October 2023

Introduction

Exploring the Park Gilpin Clear Creek real estate landscape, October 2023 unveils pivotal trends and insights. Our report covers median close prices, active listings, sales numbers, and pricing strategies, offering a comprehensive view for stakeholders.

Area Overview

In Gilpin County, Central City and Black Hawk stand out as historic mining towns, renowned for their casinos and rich history. Clear Creek County is highlighted by Idaho Springs, Georgetown, and Silver Plume, known for hot springs and charming historic districts. Park County’s Fairplay, Alma, Hartsel, and Lake George offer historical significance and scenic beauty. These areas collectively add to the unique character of the region.

Median Close Price Analysis

This October, the median close price in Park, Gilpin, and Clear Creek Counties showcased a significant rise, reaching $562,500, indicating a growing trend in property values.

Active Listings Trends

Active listings in October numbered 324, a slight decrease from the previous month but an increase from last year, highlighting the dynamic nature of the market.

Sales Volume Insights

The sales volume in October remained steady, with 90 transactions, demonstrating consistent market demand.

Pricing Strategy Overview

The close price to original price ratio in October was 94.8%, reflecting the ongoing pricing trends and market dynamics.

October 2023 Denver Real Estate Market Insights and Trends

Denver Real Estate Market Overview – October 2023

October 2023 in the Denver Real Estate market has shown significant changes. This analysis dives deep into the statistics and their implications.

Metro Denver: A Diverse and Dynamic Region

Metro Denver encompasses Adams, Arapahoe, Broomfield, Boulder, Jefferson, and Douglas Counties. Each county boasts unique characteristics, contributing to Denver’s appeal as a real estate hotspot. The region is home to major cities like Boulder, Aurora, and Centennial, known for excellent school districts and a blend of urban and natural environments.

October 2023 Market Highlights

October 2023 saw the median close price in Denver rise to $589,990, a significant increase from $575,000 in October 2022. This 2.61% year-over-year growth indicates a steadily appreciating market. However, compared to September 2023, where the median was $591,000, there’s a slight month-over-month decrease, suggesting a momentary stabilization in prices.

Active Listings and Inventory Changes

The number of active listings dropped to 8,577 in October 2023 from 9,586 in October 2022, a 10.53% decrease, reflecting a more competitive market with fewer options for buyers. Compared to September 2023, the listings decreased from 9,261, indicating a tighter market month-over-month.

Sales Trends: A Closer Look

Sales numbers in October 2023 stood at 3,375, down from 3,794 in October 2022, showing an 11.04% year-over-year decrease. This decline might indicate a market cooling or buyer hesitation. However, the slight decrease from September 2023’s 3,609 sales suggests a stable purchasing trend.

Price Negotiation Dynamics

The close price to original price ratio in October 2023 was at 98.20%, slightly up from 97.30% in October 2022. This increase suggests that homes are selling closer to their asking prices, indicating a market favorable to sellers. The month-over-month change from 98.50% in September 2023 shows a slight shift towards buyers.