UWM is paying for a 1-0 temporary buydown right now. It drops a buyer’s first-year mortgage rate by a full percentage point. No out-of-pocket cost. On a $600,000 loan, that’s about $280 a month, or roughly $3,400 across the first 12 months. There’s a real trade-off: a slightly lower permanent rate exists without the buydown. The break-even between the two is around 3.5 years. The 10-year Treasury is back near where it was a year ago. The odds of a refinance window opening before then are good. For a West Seattle or Burien buyer stretching to make a $600,000 purchase work, that first-year breathing room can be the difference between buying now and waiting twelve months.

What the UWM 1-0 Buydown Actually Does

UWM is running an aggressive promotion. It’s a “Free” 1-0 temporary buydown they fund out of their own pricing margin. The mechanics are simple. For the first 12 months, the buyer pays as if their rate is 1% lower than the note rate. In Year 2 through Year 30, the full note rate kicks in. The subsidy sits in an escrow account at closing and pays the difference each month during Year 1.

UWM is funding the buydown. It does not come out of the buyer’s pocket. It does not eat into a seller credit. It does not require any negotiation in the purchase contract. From a buyer’s cash-to-close perspective, it is genuinely free.

How Much Does It Save in Year One?

On a $600,000 loan, the 1-point rate reduction is worth roughly $280 a month in lower principal and interest. Over 12 months that totals around $3,400. Real affordability relief in the first year — when buyers are also absorbing moving costs, furniture, and repairs that nobody quotes them on the GFE.

For a buyer on the fence because the monthly payment was just outside their comfort zone, this changes the math. It reframes what’s actually affordable in the first year of ownership.

Where’s the Catch? The Real Trade-Off Against the Permanent Rate

Calling it Free is technically accurate from the buyer’s side. It is not free in the absolute sense. UWM is spending pricing margin on the Year 1 subsidy that could otherwise have gone toward a slightly lower permanent rate. On the same rate sheet, the same buyer can typically lock about a quarter-point lower rate for the full 30 years. No buydown, no Year 1 cushion. Just a permanently cheaper payment.

So the choice is a real trade-off. Year 1 cushion versus permanent monthly savings over the life of the loan. Anyone telling a buyer it is a no-brainer either way is oversimplifying.

When Does the UWM 1-0 Buydown Win?

The break-even between the buydown and the lower permanent rate works out to roughly 3 years 7 months. If the buyer refinances or sells before then, the buydown wins. If they hold the loan past that point, the lower permanent rate pulls ahead. And stays ahead for the rest of the term.

The math is straightforward. The buyer banks about $3,400 in Year 1 with the buydown. Then they pay roughly $110 a month more than they would have on the lower permanent rate, every month after that. Those $110 chunks chew through the $3,400 head start over about 31 months in Year 2 onward. Total time to break even: 12 plus 31, or 43 months.

Why a Refi Window Inside 3.5 Years Is More Likely Than Not

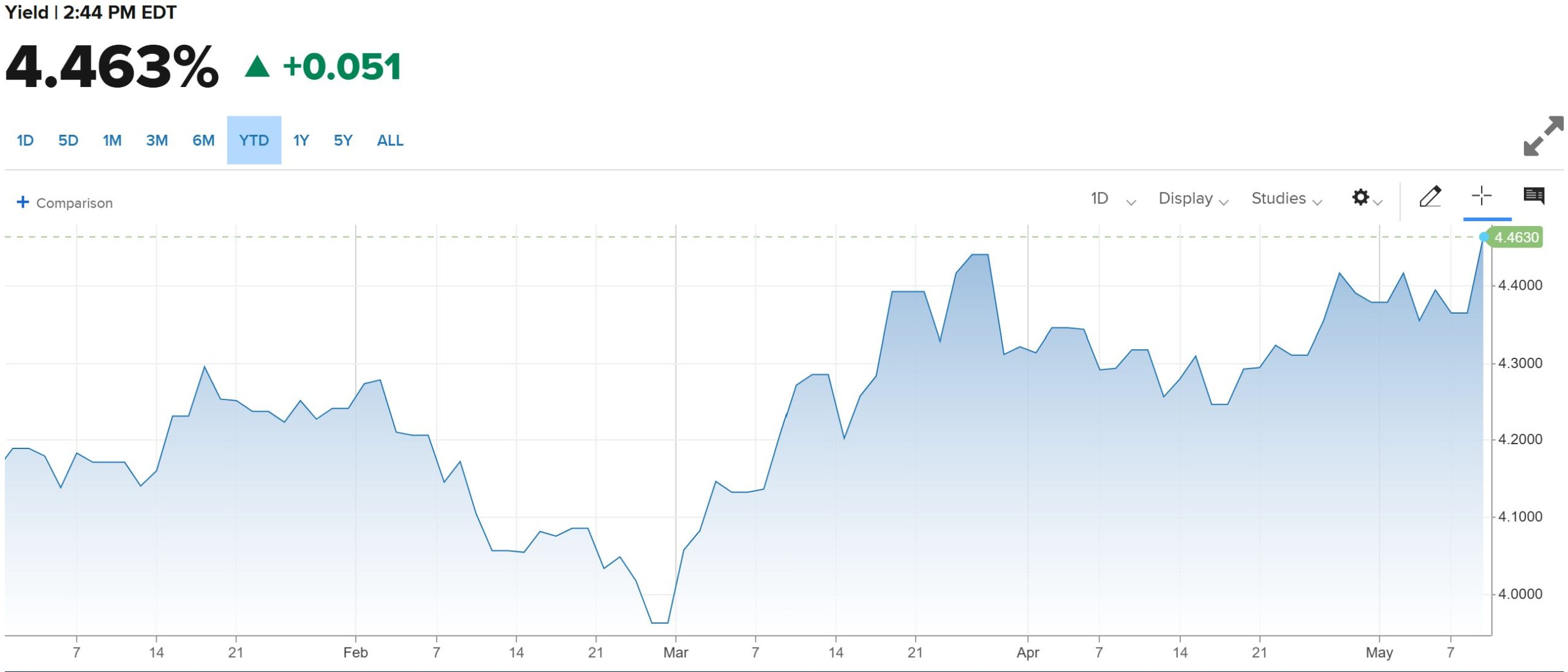

This is where the timing question matters. The 10-year Treasury drives mortgage rates more than any other single input. It closed at 4.46% as of mid-May. That’s up from a late-February low near 3.97%. That’s roughly half a percentage point of upward move in about ten weeks. It puts the 10-year right back near where it was a year ago.

The directional implication is simple. There’s real room for the 10-year to fall back toward that February low. That happens if economic data softens or the Fed signals more accommodation. Most major forecasters expect 30-year fixed rates to drift lower through late 2026 and into 2027. That includes the Mortgage Bankers Association and Fannie Mae. Whether the move is gradual or sharp depends on the data, but the directional consensus is clear.

For a buyer choosing between the buydown and the lower permanent rate, that backdrop tilts the decision. A refinance opportunity opening in the next 24 to 36 months is more likely than not. That’s well inside the 3.5-year break-even window where the buydown wins.

How to Frame the Math for a Client on the Fence

The buyer needs three pieces of information to make this decision. None of them are about the buydown itself:

- How long they realistically plan to hold the loan. The median U.S. homeowner stays put for 11.8 years. But the average mortgage only lives 5 to 7 years — because refinances end loans too. If they refi inside 3.5 years, the buydown wins.

- What their cash-flow priorities look like in Year 1 specifically. First-year homeownership tends to be the most cash-strained year for any new owner — especially for Puget Sound buyers absorbing property taxes that are higher than what their lender estimated. The $3,400 Year 1 cushion has different value to a buyer who’s stretched than to a buyer who isn’t.

- Their rate forecast posture. If they believe rates are flat or rising for the next several years, the lower permanent rate looks better. If they think rates are likely to drop and they will refinance, the buydown looks better. The 10-year’s recent move suggests the latter is plausible.

The math is not the hard part. The judgment about which lever to pull is. That is the conversation worth having before lock day.

FAQ

Is the UWM 1-0 buydown actually free?

Free from the buyer’s perspective — they pay nothing out of pocket for the buydown. UWM funds it from their pricing margin. The trade-off is that the same buyer could lock a slightly lower permanent rate without the buydown. So while there is no upfront cost, there is an opportunity cost compared to the alternative permanent rate.

What is a 1-0 temporary buydown?

A 1-0 temporary buydown means the borrower’s effective interest rate is 1 percentage point lower than the note rate for the first 12 months. After that, it steps up to the full note rate for Year 2 through Year 30. The Year 1 subsidy is funded by a lump-sum credit at closing. That credit sits in an escrow account. It pays the lender the difference each month during the buydown period.

How much does the UWM 1-0 buydown save on a $600,000 loan?

On a $600,000 loan, the 1-point reduction is roughly $280 a month in lower principal and interest. That runs for 12 months, or about $3,400 in total first-year savings. The exact figure varies slightly based on the underlying note rate, but the order of magnitude holds across the typical conventional loan range.

What happens if the borrower refinances during Year 1?

If the loan is refinanced or paid off before the 12-month buydown period ends, any unused buydown funds in escrow are typically applied as a credit toward the new loan. Or returned to the borrower per the lender’s specific buydown agreement. The funds do not disappear, but the exact treatment depends on UWM’s program terms. Verify in writing before the loan closes.

When does the buydown beat the lower permanent rate?

The break-even sits around 3 years 7 months on a typical loan. Hold the loan less than that, and the buydown wins. Hold it longer, and the lower permanent rate wins. Many mortgages do not survive 3.5 years anyway. Between refinances and home sales, the average mortgage lifespan in the U.S. is 5 to 7 years. Many end sooner when rates drop.

The Bottom Line

UWM’s “Free” 1-0 buydown is a meaningfully good product right now. Not because it’s free in the absolute sense. Because the current rate environment makes the trade-off lean in its favor. The buyer gets real Year 1 relief. The cost is borne by the lender. The break-even falls well inside the window where most mortgages get refinanced anyway. For a buyer on the fence about whether the monthly payment works, this is the kind of product that moves the needle.

The trade-off against the slightly lower permanent rate is the conversation worth having before the buyer commits to either path. Run the numbers on their actual loan size. Ask the right questions about how long they plan to keep the loan. The right answer is almost always specific to the buyer, not the product.

Related reading: how UWM’s 0% down product is qualifying more buyers. Also: the questions to ask a lender about a pre-approval. And how a reverse 1031 lets clients buy before they sell. For broader options, the full loan menu is here.

If you have a client weighing affordability options, or deciding between a temporary buydown and a permanent rate, send them my way. Happy to walk through the math on their specific loan.

Don’t just take my word on the UWM 1-0 buydown

If you want a read on how I work with clients before sending one my way, here’s where past borrowers and partners have weighed in:

Follow along:

If you have a client weighing the UWM 1-0 buydown against a buy-down of the permanent rate, send them my way. We’ll run the actual numbers on their loan size, target rate, and realistic hold horizon.